A THESIS: AUTONOMOUS FINANCIAL CONDUCTORS

On Financial Instruments So Consequential They Will Redraw How Governments Govern and Whether This Century Ends in Prosperity or We Squander It

Sahith Aula | General Partner, Katha VC | March 2026 | V2

M.Phil., University of Cambridge | J.D., Arizona State University | B.A., Emory University | 2 decades across investment law, hedge funds, and building fintech

Disclaimer: This thesis is intended for accredited and professional investors only.

“The most profound technologies are those that disappear. They weave themselves into the fabric of everyday life until they are indistinguishable from it.”

- Mark Weiser, Chief Scientist, Xerox PARC

The greatest transfer of economic power in human history is underway, and most of the investor capital in the world is looking in the wrong direction.

There are 1.4 billion adults on this earth who have never held a bank account. Not because they lack transaction history or need, but because the financial system simply never reached them. This is not about charity or social impact investing. It is the largest unpriced market opportunity in the history of finance, and the data infrastructure to serve it, through local emerging markets startups, has only arrived recently.

What has also arrived, largely unrecognized outside a small circle, is the class of systems that will ultimately direct that infrastructure, Autonomous Financial Conductors. They are sovereign, domain specific intelligences that will, in the near future, conduct the economic life of nations, businesses, and households the way a conductor shapes an orchestra...anticipating, coordinating, and correcting in real time. I will show you, in this essay, why I believe they are inevitable and investable.

You see, the clearest early signal did not show up in a fintech earnings call. It showed up in war.

Last week, at the time of my updating this version, in the early hours of March 3rd, 2026, the United States and Israel executed nearly 900 strikes on Iranian military and nuclear sites in under 12 hours. AI targeting systems (Palantir’s Maven, Anthropic’s Claude, and Hasbora) drawing from drone feeds, satellite imagery, and communications intercepts compressed what once required weeks of human deliberation into something closer to a blitz. The Wall Street Journal described it : AI tools were central to “gathering intelligence, selecting targets, planning airstrikes, and evaluating damage at previously unattainable velocities.” Bloomberg called it “a large scale test for AI assisted warfare.”

Just 4 years ago, OpenAI’s ChatGPT was only scoring in the 90th percentile on the law school entrance exam (LSAT). And now it is determining the intricacies of war on a live basis. The pace of AI’s development is incomprehensible

The race to Artificial General Intelligence and later Superintelligence is not theoretical...it is in our sights. But this essay is not about that race. You see, compared to Ilya Sutskever, Demis Hassabis, or Yann LeCun, my years across the many facets of financial services prepared me for an entirely different exam in an entirely different world. I will leave those predictions about to people who have earned the right to make them. What I know is financial services.

Perhaps only after healthcare, in my view, is financial services the most consequential sector. Because financial services is the circulatory system of civilization. It determines how people earn, save, and gather wealth, how businesses access capital to grow, how economies allocate resources across generations and across every instrument in the human toolkit, from the simplest savings account to the most intricate derivatives.

What I know about financial services tells me that the next 15 to 20 years will produce the most remarkable expansion of financial access, economic transformation, and broadly shared prosperity in recorded history.

I am certain of this. That is what this essay is about.

ప్రేమతో dedicated to my parents.

I. THE RACE AND THE STRUCTURAL REALITY

The architecture of the next century is being drafted by a handful of scientists and politicians whose choices will bind the rest of the world’s future.

At this point many, but not most, people in the cosmopolitan monoculture globally understand this but feel too marginal to influence the outcome.

Artificial General Intelligence (AGI), as I understand, refers to an AI system capable of performing any intellectual task a human can, across domains, rather than the narrow applications today’s systems are optimized for. Superintelligence is what follows. It is an AI that surpasses human cognition by a measure so vast it becomes functionally incomprehensible to us. Leopold Aschenbrenner’s analogy, from Situational Awareness, is the one I cannot shake from my own mind. The leap from AGI to Superintelligence mirrors the leap from the atomic bomb to the hydrogen bomb.

In fact, the atomic bomb was already the most devastating weapon in human history. The hydrogen bomb made it look like a firecracker and delivered more destructive intensity than every weapon fired across the entirety of the Second World War combined.

That is the chasm we are crossing.

That chasm, according to many observers, may be bridged within this decade. Whether that bridge is crossed in seven years or seventeen, I’m uncertain because my field is financial services (though do give me some leeway for international affairs as that was my field for many years as well).

Now, the United States and China are the undisputed principals in this game. America has made a largely unspoken but unmistakable wager: prioritize capability, move aggressively, and treat regulatory friction as a competitive liability. China’s posture is semi-state-directed, long horizon, and organized around the conviction that AI is national infrastructure rather than a commercial venture. DeepSeek demonstrated in 2025 that China could produce frontier caliber models at a fraction of the assumed cost and release the methodology publicly. That strongly signaled they had already advanced well beyond it internally. Whoever achieves AGI first will hold something approximating what nuclear weapons represented in 1945, and the capital that backed the right platforms on the way there will own claims on some of the most powerful economic engines ever built.

This is great if you are an OpenAI or Anthropic or Google investor. However, there is a dimension of this race that almost no one is discussing candidly. The AI that wins will not be a neutral tool. It will carry the legal assumptions, cultural values, governance philosophies, and social frameworks of the civilization that built it. When a system trained overwhelmingly on country X’s legal precedent, its values (or those of its AI scientists), its contract norms, and its behavioral economics gets deployed into Brazilian courts, Filipino monetary policy, or Indian property registrars, it does not arrive as a blank instrument. It arrives as a foreign system embedded in an algorithm. The nation that believes it has adopted cutting edge AI governance has, de facto, outsourced the definition of justice, creditworthiness, and economic rationality to someone in a different hemisphere who has never set foot in the country being governed.

This is not a theoretical concern. It explains why the question of who builds the AI that governs a nation’s financial life is not merely a national security matter. It is the difference between self determination and the most sophisticated form of dependency. The latter is outright not acceptable to a major government, even if they will gladly accept foreign investment into these critical companies (just like the US and China both do due to the sums required). And so, I will put what I expect to happen in the next few years very plainly: there will not be just one AI that rules them all globally. The major 20-30 sovereign nations will move to build or back their own systems, locally. The global investors who read the landscape correctly will back them first. Extraordinarily, nearly all of them will, in my view, be available for investment by global investors just like Americans can invest in Chinese publicly traded AI companies and vice versa.

We must now take a step back though and dive a bit deeper on why those 20-30 sovereign nations will not accept a handful of corporations from other countries, whether state directed or otherwise, from becoming the dominant forces in their ecosystems. Establishing reference points to build upon that will ultimately lead to the discussion on financial systems I expect to see in the coming decades. By that, I mean suspicion of control by foreign corporations goes back to the British East India Company or Royal Dutch Shell. And that specific fear is just as relevant to this conversation on AI as conquest by a sovereign nation. Because the largest AI companies are more powerful, already, than perhaps all but 10 nations on earth. Nations with large populations and fast growing economies will not accept that they cannot be players in the game for much longer.

Therefore, the questions that genuinely interest me, and what we will uncover in this essay, is not which country will dominate the AGI and Superintelligence races or whether corporatocracies or one party states are more durable against them. It is, what will the global and respective national financial systems across markets look like when they are remade?

II. THE WHY OF FINANCIAL SERVICES

Now, some of you may be wondering still. So let me address it. Here is why financial services ought to command more attention than any other sector in this transformation.... It is not one industry among many. It is the underlying architecture on which every other industry rests.

The credit that capitalized your employer shaped how you earn. The instruments available, or unavailable, in your neighborhood shaped how your family saves. Whether capital reaches a business, at what price, and on whose terms determines whether that business ever becomes what it could have been. The borrowing mechanisms, risk frameworks, and investment instruments of an economy are the machinery through which prosperity either accumulates across generations or dissolves. Financial services does not mirror wealth. It manufactures it, or withholds it, across every population it serves and every one it has ignored. That is the system now being remade. That is the magnitude of what this conversation is actually about.

I am a pragmatist (my collection of Murakami and RK Narayan aside). I carry fiduciary duties to investors who have certain expectations on the returns I will deliver. But, I hold a genuine conviction about what financial empowerment can accomplish for hundreds of millions of people. These are not competing positions. They are the same position, in my view.

You see, that is how durable change actually moves. It does not arrive through proclamations. It arrives through outcomes that cannot be argued away. The societies that arrive there earliest, with locally built and locally accountable systems, will compress a century of developed world progress into a single decade. One decade. Someone will write the first checks into the systems that make that compression possible. The rest of the world will call it “beta” and pretend it was inevitable.

That transformation will be most legible, most measurable, and most investable in financial services and in specific markets. Markets that, no matter your nationality, you can invest in. That is where this essay is headed.

III. THE TWO PATHS: HOW THE WORLD’S FINANCIAL TECHNOLOGY SYSTEMS WERE BUILT

To grasp the scale of what is approaching, you need to understand a foundational divergence in how the world’s modern financial technology systems were assembled. We need not go back to Adam Smith’s era of when he wrote the Wealth of Nations nor the Bretton Woods Conference either. Because we’re highly focused on when true financial technology came to be, in the 1980s, and what that meant for the world. At Katha VC, we call this the Fintech Ecosystem Evolution Path and I developed it last year…in fact it is the basis for this very essay. I encourage you to read that Fintech Ecosystem Evolution Path paper, but I will summarize much of it here.

In that guide, I wrote how fintech ecosystems around the world follow one of two paths depending on when their core modern financial infrastructure developed (i.e. the 1980s vs. the 2010s). This dual track perspective, ultimately converges in their respective 5th stage of Autonomous Financial Intelligence and Conductors.

Path 1 traces the trajectory of the United States, Japan, and Europe. These economies erected elaborate physical financial infrastructure first. They built branch networks, ATM grids, card payment systems, and credit bureaus that anchored Stage 1.1. Financial services demanded physical presence. Payments traveled through cards or wire transfers with settlement windows that ranged from two to seven days. Small businesses navigated relationship banking and manual underwriting processes.

These systems digitized incrementally through Stage 1.2. Online banking and early mobile applications emerged alongside the early internet. From there came Stage 1.3. Sophisticated financial products, algorithmic trading, and wealth management platforms spread across the socioeconomic spectrum. APIs stitched services together. Embedded finance allowed fintechs to coexist with entrenched institutions. Real time payments arrived with almost comical delay. FedNow launched in the United States only in 2023, decades after the infrastructure was theoretically within reach. That is rather brutal when you think about it. Decades.

Path 1 countries now occupy Stage 1.4, the era of AI augmented finance. Machine learning drives credit decisioning, fraud detection, and portfolio construction. Smart contracts are beginning to automate complex transactions. Robo advisors have reached the mass market. Predictive analytics and automated compliance are becoming routine for small and medium enterprises.

Path 2 tells an entirely different story. These are the high growth markets: India, Brazil, Indonesia, Nigeria, Egypt, Mexico, Kenya, Vietnam, the Philippines, and the Gulf states. Many began at Stage 2.1 as something close to a tabula rasa. Branch networks outside urban centers were sparse. Cash dominated. There were no widely functioning credit bureaus. Banking was unavailable to more than 90% population.

Then something remarkable happened. Rather than retracing the 40 year digitization journey of Path 1, these markets bypassed it entirely. They reached Stage 2.2 by boldly and aggressively building digital identity systems first. Aadhaar in India is the defining model. On top of that came mobile money platforms and real time payment rails that were constructed from scratch, often with government backing: UPI in India, PIX in Brazil, M Pesa in Kenya. The result was mass account creation via mobile, peer to peer transfers, and genuine financial access, all on infrastructure that is more modern than anything in the developed world. These countries did not inherit the old system. They engineered a better one.... From there, these markets assembled Stage 2.3. Embedded finance and comprehensive services became the norm. Super apps like Paytm integrated lending, insurance, savings, and investment into unified platforms. Credit extended through transaction data and alternative scoring reached borrowers with no formal credit history whatsoever. Real time cross border corridors opened for diaspora remittances.

The most advanced of these markets are now moving into Stage 2.4. AI pilots are emerging across mature fintech verticals. Many companies are approaching IPO scale as multibillion dollar enterprises. Regulators are growing more adaptive. Machine learning is augmenting credit decisioning, fraud detection, and risk pricing in ways that were inconceivable a decade earlier.

Because Path 2 markets built their infrastructure from scratch on contemporary rails, they are not merely closing a gap. They are pulling ahead. The transaction level behavioral data now accumulating on populations that were previously invisible to the formal financial system is richer, more granular, and more current than anything the developed world has gathered across decades of legacy system operation. Risk frameworks trained on this data will surpass anything Wall Street has constructed. They will do so because they have observed the full range of human financial behavior, not merely the portion that was already banked. That data advantage, deepening with each passing year, is the bedrock on which the most consequential financial innovation of the next two decades will be erected.

The Path 1 and Path 2 divergence is not a historical curiosity. It is the central investment thesis of the next decade. Path 2 markets carry substantially higher long term upside precisely because they started from less, built cleaner, and are now layering AI on infrastructure that in many cases surpasses anything implemented in the United States. This is where the real arbitrage lives. Most large pools of capital are still priced for Path 1. The mispricing is in Path 2.

For an allocator managing a family office, this matters for one simple reason. In Path 1 you are mostly paying for efficiency gains on an old stack. In Path 2 you are financing the first serious drafts of entirely new stacks. Efficiency compounds, but origin creates the possibility of outsized gains that cannot be replicated by tuning someone else’s system.

IV. AUTONOMOUS FINANCIAL CONDUCTORS: THE INVESTMENT OF A GENERATION AND FOR POSTERITY

At this point, I must say, thank you for staying with me. It may have felt winding, but I needed to set the rails for this discussion while also bantering a bit about the core. And this section is truly the core of what I want to say.

Consider what we have discussed herein until now. AGI and Superintelligence. Democracies and One Party States. Globalized and dominant AI companies and localized, sovereign supported, AI companies. And, of course, the evolutionary path that financial technology systems have taken and the vaulting that has occurred. Now, let’s begin.

In 15 to 20 years, the world’s financial systems will not resemble more polished versions of what we have today. They will be categorically and structurally different. The entire social contract (whether Hobbesian or Confucian or something else entirely) will be rewritten. What I call an Autonomous Financial Conductor, Stage 1.5 in Path 1 markets and Stage 2.5 in Path 2 markets, is not an incremental upgrade. It is the difference between our singular Sun in our solar system to the millions of stars in our Milky Way Galaxy...it is that astounding.

However, before describing what it does, I need to be precise about what it is. The emergence of Autonomous Financial Conductors will not mean that every government will build its own national AI from scratch. Most will not. The prima facie assumption that sovereign AI requires state built AI misreads how this will all actually unfold.

Governments, especially emerging markets governments, will do something else. They will establish, as a matter of explicit national priority, that a local player must dominate locally in key domains.

These domains include economic policy guidance, credit allocation infrastructure, judicial analytics, welfare distribution, and financial regulation. It is hardly far-fetched when you consider the US Government defense contracts that Google, Microsoft, Palantir, and OpenAI all have in the US. The state sets the mandate and the legal environment. It establishes the data sharing frameworks. It ensures that the entity conducting these functions is locally owned, locally accountable, and built on locally sourced intelligence. The conductor will quite likely be built out of a well financed local fintech startup. It will not be foreign controlled. That is not bad news for global investors. That is, in fact, the moat.

This distinction, between sovereign AI and locally dominant AI, is subtle but decisive. It transforms the picture because the state has every incentive to defend the local conductor’s position once it becomes embedded in monetary policy, credit allocation, and welfare delivery. In practical terms, that means governments will end up defending the franchise value of the very companies early investors backed.

From India to Brazil, these massive countries with immense talent and economies will build their own. They may not be on par with Palantir in technological capacity. But they will be publicly traded, regulatorily insulated, hundred billion dollar market cap companies in their own right. After all a Toyota Camry might not be a McLaren supercar but it is unparalleled in its reliability and is an exceptional piece of engineering in its own right.

The opportunity belongs to the founders who build these systems and to the family offices, from New York to Singapore to Mumbai, that recognize they are not buying into a feature. They are buying into infrastructure their host governments will eventually be unable to govern without.

Now. Finally. I can describe what a sovereign’s Autonomous Financial Conductor will look like in practice.

A nation’s financial AI will, ultimately, be its economic constitution. It encodes who gets credit and who does not, what constitutes risk and what does not, how welfare flows and how capital accumulates. Those decisions must reflect local legal traditions, local behavioral economics, local community structures, and local priorities. Something so critical, so staggeringly impactful can only be equated to a Manhattan Project.

At the consumer level, a person living in a Stage 2.5 economy does not interact with financial services the way anyone does today. There is no application to log into. There is no form to complete. There is no credit request to submit. An AI financial conductor, embedded in the digital identity infrastructure that already knows this person, manages their financial life proactively. It routes idle cash into yield instruments automatically. It recalibrates insurance coverage in real time as life circumstances shift. It detects a looming cash flow gap six weeks before it arrives and a priori positions a credit facility to absorb it, priced according to this person’s actual repayment behavior across years of transaction data. It does not rely on a score generated by an algorithm that has never encountered their economic reality.

Retirement is no longer a burden this person must carry alone. Across an entire working life, a managed account allocates on their behalf. It rebalances and compounds the way private wealth management has served the ultra rich for a century. Now the same capability is available to a market vendor in Lagos or a factory floor worker in Surabaya. Finance recedes from friction to infrastructure. Most people alive today have never experienced anything close to this. Most people alive in 2040 will regard it as unremarkable. How wild.

From an investor’s perspective, that is not a product description. It is what happens when private bank level service becomes the default setting for hundreds of millions of people who were previously disregarded by the system. The fee pools and data streams that follow will not be small.

At the SME level, a small business owner in a Stage 2.5 economy has an AI treasury function that does not rests. Overnight, it has settled three supplier invoices via cross border rails at negligible cost. It has swept surplus liquidity into a short duration yield position. It has flagged a receivable showing early delinquency signatures based on counterparty transaction patterns. It has pre positioned a currency hedge ahead of a volatility window identified in central bank communications. The owner requested none of this. The system is oriented around the business, not the reverse.

Treasuries like this do not stay confined to one firm. Once proven, they become standard. Whoever owns the conductor that runs them does not own a niche. They own the whole damn thing.

At the macroeconomic level, the story becomes more dramatic, if it were possible.

A Stage 2.5 economy does not calibrate interest rates through a committee of central bankers who convene monthly, read prepared remarks, and vote according to some mixture of economic models, political pressure, and personal conviction. It receives recommendations generated in real time from a system that has absorbed every transaction in the economy, every employment signal, every price movement at every tier of the supply chain, every housing listing, every food price at every market stall, every remittance corridor, every loan default, and every savings balance. The output is not ideology. It is empirics. AI conduction delivered to central banks and finance ministries will eventually be so empirically precise, so consistently superior to whatever the committee produced, that even the most resistant institutions will quietly begin following it. They will not do this from ideological conviction. They will do it because the results are undeniable and visible to the populations they serve. Verdad, no?

When that happens, the conductor is no longer just another system vendor. It sits at the same table as the central bank. Investors who were early do not just own equity in a company. They own a piece of the country’s decision engine.

What elevates this from impressive to essential is simple. That conductor must be built by people who understand the economy it is governing. It must be built by people who know the actual texture, not just the aggregate statistics. A system constructed in California, however powerful, will process these realities as noise or as outliers to be smoothed away. A system built in Mumbai or Cairo or Jakarta by founders who grew up inside these economies will recognize them as the signal. It is the difference between a governance tool and a governance liability. It is the reason why the national priority in each of these markets will not be to adopt the best global AI. It will be to ensure that the best local AI dominates the functions that define sovereignty.

For investors, that is the filter. The right bet is not “any AI” in an emerging market. It is the local conductor that treats these so-called edge cases as the main event.

It is worth stating plainly who benefits from this in capital terms. AI fintech companies that can see this clearly into an economy, and that governments come to rely on, are not disposable vendors. They become core infrastructure. Their cash flows, and their data advantages, tend to be very hard to dislodge. Ultimately, nations that write that specification themselves, calibrated to their own legal traditions, their own cultural realities, and their own on the ground truths, will govern their own futures. Generalist AI will not execute on this. The financial conductors will. Global investors who grasp that distinction, and recognize the margin of safety of riding the wave rather than going against it, will likely earn returns that reflect it.

And so, the societies that leapfrogged the legacy banking system will leapfrog the legacy economic policymaking apparatus as well. They will do it more completely and more rapidly than anything the developed world has achieved, precisely because there is far less institutional inertia to displace. Let us consider a clear example

VI. INDIA: THE GOLD STANDARD OF LEAPFROG POTENTIAL

India has everything. The talent is formidable and the manpower is...sizable to say the least. A Government that has ruled for over a decade and has made the country more significant on the world stage. The country has world class engineers, mathematicians, and AI researchers who rank among the finest anywhere. UPI processes roughly 180 billion dollars in transactions every month and has become a global reference point for real time payment infrastructure. The India Stack, including Aadhar, is among the most ambitious pieces of digital public infrastructure ever assembled by any government.

And yet.

Navigating a property registrar’s office in India routinely requires a bit of influence. Government tasks that should resolve in hours drag on through bureaucracy and low productivity standards. And I do not mean in some distant rural backwater but everywhere, habitually, as an unremarkable feature of daily life. The welfare for votes dynamic persists. The regulatory environment, despite genuine improvement, remains a labyrinth due to the vast bureaucracy that punishes precisely the kind of capital light and fastmoving innovation that the coming generation of AI driven financial companies will require.

None of that is the end of the story though.

You see, the trendline is shifting faster than most outside observers have acknowledged. Immigration headwinds in the United States and Europe are eroding the calculus that once made departure of talent feel inevitable (my own family was amongst the earliest wave in the 1970s to Canada and later the United States). State governments like Andhra are competing ferociously for talent and investment with a seriousness that would have been unrecognizable a decade ago. The quality of urban professional life in India has improved beyond recognition, and a growing cohort of world class engineers wants to build at home. Not out of obligation.

Because the opportunity has finally materialized to justify it.... What is most significant about India, though, is a dimension that rarely surfaces in Wall Street investment analysis. The country faces an urgent and strategic need for locally dominant AI. India has 22 constitutionally recognized languages. It has credit behavior shaped by joint family financial obligations that bear no resemblance to the individual credit models embedded in international scoring systems. It has an informal economy representing roughly half of GDP, operating on trust networks and social collateral that no FICO style algorithm was ever designed to read. It has regionalist dynamics that silently distort access to capital in ways that neither a dataset assembled in Palo Alto nor a model trained on English language financial records will ever detect. The AI that governs Indian monetary policy, adjudicates Indian contract disputes, and allocates Indian welfare resources must be built by people who understand these realities from the inside. It must be calibrated on data that reflects them honestly, or it will fail.

India is highly unlikely, in my view, to mandate that government agencies build this AI (even the Indian government is acutely aware of how excruciatingly bureaucratic its own institutions can be). The far more likely path is that India decides, as a matter of explicit national priority, that a local player must dominate locally in key facets of economic policy, financial regulation, and judicial governance. This herculean effort can only be executed on as a national priority on the scale of the Manhattan Project.

This means, the state sets that mandate. It protects the underlying sovereignty. The execution comes from Indian founders, Indian engineers, and Indian companies that carry the cultural fluency and on the ground knowledge no imported system can replicate. This is not protectionism. It is self determination expressed as technology policy. It is the model that every serious emerging market will eventually follow. For investors, Indian or American or otherwise, that is not a closed door. It is a very specific invitation. The capital that partners with those founders early, on terms that respect local control, will sit inside the apparatus that future governments will quietly rely on.

The Autonomous Financial Conductors, that will be built, will be specifically engineered to route around India’s institutional failures. They will replace politically compromised committee decisions with empirically grounded ones that are too publicly visible to dismiss. AI underwriting in India already serving borrowers at meaningful scale, has already demonstrated what leapfrogging of more developed nations looks like in practice. What follows is the compounding of that foundation at a pace no legacy market can approach, precisely because there is so much more terrain to traverse and so much urgency driving the journey.

The gap between what India’s governance delivers today and what its population is capable of is not just a criticism. It is the exact contour of the opportunity.

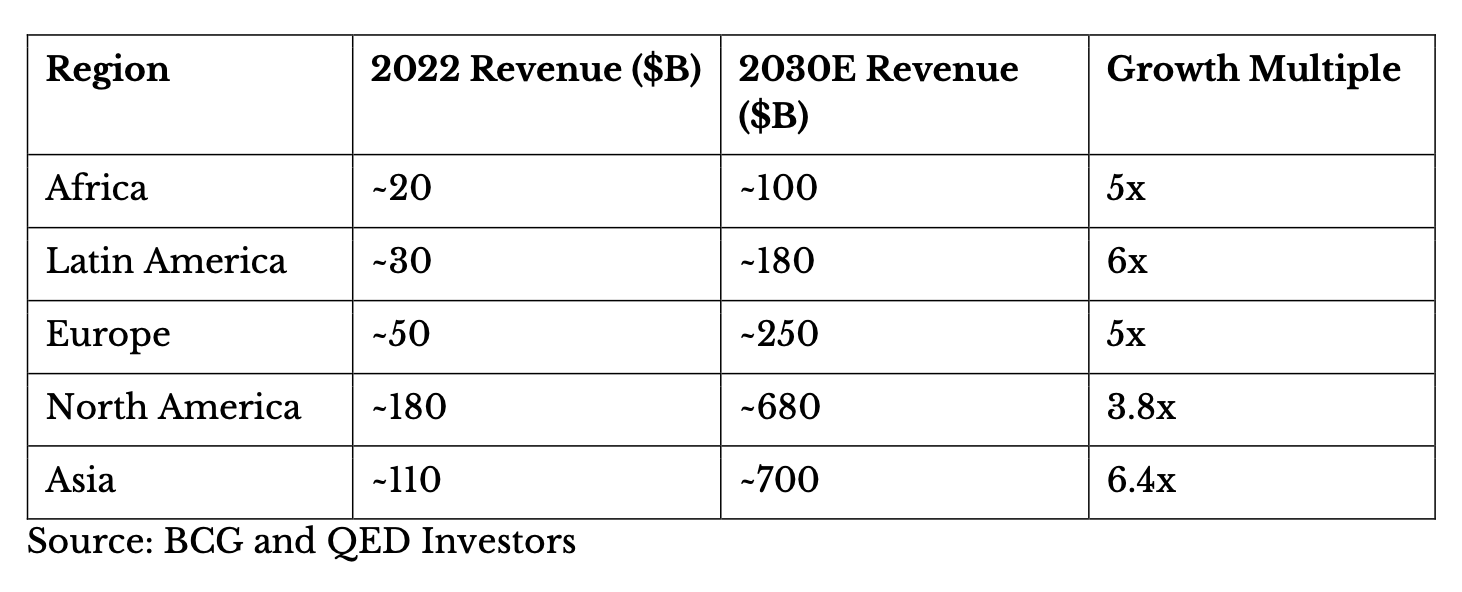

VI. THE NUMBERS: WHY EMERGING MARKETS FINTECH CANNOT BE IGNORED

The scale of what is approaching is best understood through the revenue trajectory of global fintech. It reflects the volume of financial services being intermediated by technology rather than traditional banks.

The highest multiples belong to the markets most investors overlook. The demographic momentum is stronger. The infrastructure is newer. The result is that the same quantum of innovation produces more visible growth.

Whether due to lower costs of living or sheer ability to execute with less. the capital efficiency of emerging market fintech is not an anomaly. It is the defining characteristic of the asset class. These ecosystems are simply underfunded. That gap is not self correcting. It persists because of home bias among global investors who have never sat across a table from a founder in Lagos or Jakarta and saw what it means to be constructing the financial architecture of a society that is bypassing an entire generation of legacy systems at once. That should be incredible exciting for those of us who love fintech.

This is not an argument that Silicon Valley lacks compelling opportunities. Of course not! It has extraordinary ones that simply cannot be found elsewhere…at least not for 2-3 more years. A substantial portion of capital flowing to Silicon Valley, however, funds minor refinements on what already exists. We all know it. Many of these companies are incremental iterations dressed in the vocabulary of disruption. Not to mention the bloat in salaries has ironically led to some AI replacing its very developers.

But that dynamic is largely absent in emerging markets. When a founder in Sao Paulo or Manila builds a fintech company, it is because the alternative is nothing. There is no incumbent to and no legacy product to iterate on. What they construct either creates something genuinely new or it does not exist at all. That constraint produces a categorically different quality of disruption. It is more foundational, more durable, and ultimately more valuable.

VII. THE VISION FORWARD

The most consequential financial services investments of the next decade are not taking shape in London or New York. They are in Amaravati, Nairobi, São Paulo, and Ho Chi Minh City. They are early stage companies that are building the financial infrastructure that will underpin the Stage 2.5 world described in this essay.

They are building the foundational infrastructure for the autonomous financial conductor of their nations. And more likely than not, one of these fintechs will become that very Autonomous Financial Conductor for its country.

Think about it. These startups are building functions that include credit allocation, monetary guidance, judicial analytics, and welfare distribution. The fintech founders in Mexico City who are engineering credit scoring from mobile transaction data are building the behavioral economics layer that will eventually inform Filipino monetary policy. The founders in Jakarta who are building embedded insurance are assembling the actuarial foundation on which Indonesian welfare automation will rest. These are not metaphors. They are the literal sequence in my mind. The data infrastructure comes first. The AI conductor layer follows and then leads.

We will witness multiple Manhattan Projects of financial services, and they will form globally. Those who take the leap today are not making a narrow thematic bet on emerging markets. They are aligning themselves with the financial architecture that will govern how billions of people earn, save, borrow, and invest. They are taking positions in the companies that, in many of these markets, will become as central to daily economic life as the central bank itself. And you will know I am right when an emerging markets “fintech startup” quietly becomes the invisible center of gravity that regulators, banks, and finance ministries orbit while they begin to redraw an entire nation’s financial system within the next few years.

I want to end this essay not with a warning on AI, as so many do, but with something I genuinely feel...excitement.

The kind of excitement that keeps you up at night not with existential dread, but with the eagerness of an astronaut, the day before he takes flight, looking up at the night sky, on the verge of fulfilling those childhood dreams. And my excitement is that the greatest financial system in human history is being assembled right now, transaction by transaction, in cities of incredible talent and innovation around the world.

I look forward to meeting the moment with you.

Disclaimer: This is an educational thesis intended for accredited and professional investors only. It is not financial or investment advice. Always consult tax, legal, and investment professionals before making an investment.

Let me know what you think! Are autonomous financial conductors likely or science fiction?